As a core pillar of Europe’s industrial economy, the chemical industry is grappling with the most severe development crisis in its history. Beset by the dual pressures of soaring energy costs and tightened carbon emission regulations, it has seen a rapid wave of capacity shutdowns and a cliff-like drop in investment, pushing the entire sector to the brink of collapse. The EU’s plan to relax carbon emission reduction rules has emerged as the last attempt to rescue Europe’s chemical industry.

Mass Capacity Withdrawal and a Severe Investment Winter

According to a report released by the European Chemical Industry Council (Cefic) on January 28, 2026, the capacity closed down by Europe’s chemical industry surged sixfold between 2022 and 2025, amounting to a total of 37 million tonnes, accounting for 9% of Europe’s total chemical production capacity—equivalent to the complete disappearance of the entire chemical production capacity of the Netherlands or Belgium. Among this, the capacity shut down in 2025 skyrocketed to 17.2 million tonnes, nearly a fivefold increase from the 2.9 million tonnes in 2022.

In terms of the industrial structure, the upstream petrochemical industry has been the hardest hit, with 17.8 million tonnes of closed capacity accounting for 48% of the total. Geographically, Germany, the Netherlands and the UK have become the worst-affected regions, with the combined closed capacity of the three countries making up 57% of Europe’s total. The capacity shutdowns have directly triggered an employment crisis, leaving 20,000 people directly unemployed and nearly 90,000 indirect jobs hanging in the balance. Meanwhile, investment in the sector has frozen solid: new investments plummeted by 90% from 2.7 million tonnes in 2022 to 0.3 million tonnes in 2025. The previously extensive low-carbon innovation investments have been whittled down to only a handful of pilot projects, all concentrated in the specialty chemicals segment.

Skyrocketing Energy and Carbon Costs as Core Constraints

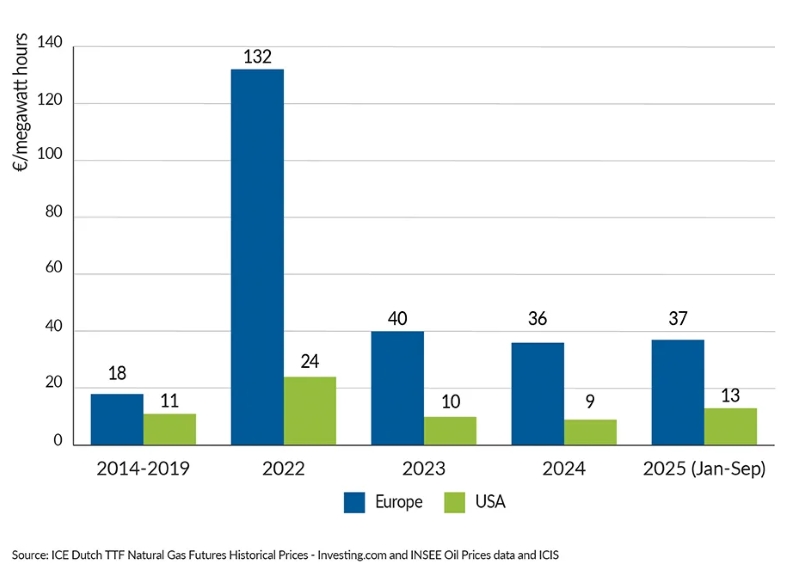

The lack of competitiveness due to high energy costs is the primary reason for the shutdowns in Europe’s chemical industry. Following the Russia-Ukraine conflict, natural gas prices in Europe have remained stubbornly high, standing at 36-37 euros per megawatt-hour in 2024-2025, three to four times the level in the US. Energy costs now account for 75% of the production costs of petrochemical products. The EU aims to completely ban Russian natural gas imports by 2027 and instead rely on more expensive US liquefied natural gas, further exacerbating cost pressures.

Stringent carbon emission regulations have added to the woes of European chemical enterprises. The EU’s “Fit for 55” plan and Carbon Border Adjustment Mechanism (CBAM) have driven up corporate compliance costs, with the sector shouldering over 20 billion US dollars in annual green regulatory costs, and 10% of capital expenditure spent solely on regulatory compliance. The EU will impose a carbon tax on imports and gradually phase out free carbon allowances starting in 2026. It is estimated that the 30 high-emission chemical enterprises in Europe will face an annual compliance cost of 6.5 billion euros, sending their operational pressures soaring, a key finding shared in the latest industry news focused on European industrial sustainability.

Faced with the industry crisis, the EU plans to relax emission reduction rules for thousands of enterprises and release the details of the reform of the Emissions Trading System in the third quarter of 2026, slowing down the phase-out of free allowances—a measure seen as the last lifeline for Europe’s chemical industry. However, the market gap left by Europe’s chemical industry is being quickly filled. China holds 67% of the global production capacity in some polymer segments, and major international players such as BASF and Dow are accelerating their capacity transfer to China. New fertilizer production capacities in Russia and the Middle East will also enter the European market in the future, further intensifying competitive pressures.

Although the EU has introduced supportive measures such as coordinated financing and accelerated approval processes, insiders believe these are far from sufficient. Marco Mensink, Director General of Cefic, stated bluntly that European policymakers have been slow to respond to the challenges facing the industry, and their pace of action lags far behind the changes in the global market. If they fail to significantly speed up their response, the decline of Europe’s chemical industry may be irreversible.

{kind=link}